Many Americans who were unable to meet the individual mandate of the Affordable Care Act by obtaining health insurance before 2014 were able to take advantage of a grace period in the last few months before a tax penalty came into effect.

However, the Obamacare extension to sign up for health insurance ends this month, which means those who are not signed up for a health coverage plan by March 31, 2014 could be charged a tax penalty.

So how should you go about obtaining health care without breaking the bank? Check out our infographic below for the breakdown.

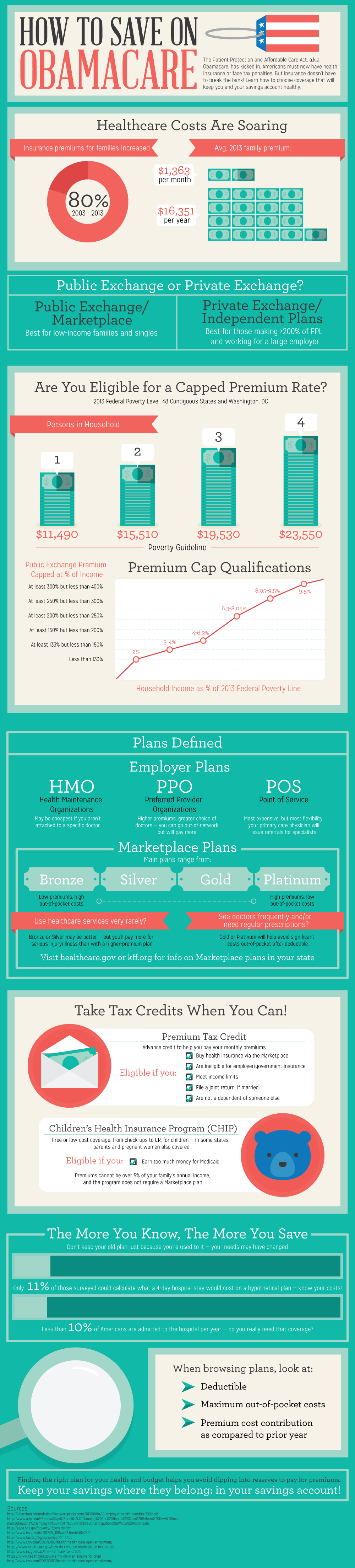

How to Save on Obamacare

Check out this comprehensive infographic on saving with Obamacare, courtesy of GoBankingRates.com.

What is the Obamacare Tax Penalty?

According to the shared responsibility provision for the Affordable Care Act, “the federal government, state governments, insurers, employers and individuals are given shared responsibility to reform and improve the availability, quality and affordability of health insurance coverage in the United States.”

Since the individual mandate under Obamacare is a major factor for the shared responsibility of paying for health insurance in the United States, the tax penalty is an individually shared responsibility fee paid if the individual does not have minimum essential coverage. The individual mandate affects about 16 percent of uninsured Americans so far within the first quarter of 2014.

In order to avoid the tax penalty that comes into effect after the Affordable Care Act extension ends, individuals must enroll in an insurance marketplace no later than March 31 of this year. Once open enrollment ends on this date, you will not be able to sign up for health insurance until Nov. 15 when the marketplace opens up once again.

How Much is the Tax Penalty?

The tax penalty for not having insurance in 2014, according to the Affordable Care Act, is either 1 percent of your yearly income, or $95 per adult and $47.50 per child — whichever is higher. The maximum penalty amount a family will pay in 2014 under the latter method is $285.

In 2015, the tax penalty increases to 2 percent of household income, or $325 per adult and $162.50 per child, with a maximum of $975 per family. In 2016, the tax penalty increases again to 2.5 percent, $695 per adult and $347.50 per child.

Starting in 2017, the tax penalty will increase annually by the rate of inflation and cost of living for each adult, child and family moving forward.

Yet, if you are uninsured for only part of the year, then one-twelfth of the yearly tax penalty is only applied to each month that you are uninsured. There is no penalty for a single gap in coverage of less than three months in a year.

Additionally, the maximum tax penalty cannot exceed the national average yearly premium for a bronze plan.

Are There Exemptions to the Tax Penalty?

There are a number of exemptions to the tax penalty, ranging from income qualifications to specific “hardship” exceptions.

If you are able to enroll in a health insurance plan through the marketplace exchange by March 31 of this year, then you will not be required to pay a tax penalty for any month before your coverage began. Additionally, if the cost of premiums is more than 8 percent of your household income, you’re exempt.

If the Health Insurance Marketplace has certified that you have suffered a hardship that prevents you from obtaining coverage, then you will not be liable for a tax penalty. Additionally, if you qualify for religious exemptions or are a member of a recognized health care sharing ministry, then you are exempt from the shared responsibility fee.

Members of a federally recognized tribe, individuals who are incarcerated and undocumented immigrants are also not required to pay the penalty fee after the Affordable Care Act extension ceases.

Overall, the Congressional Budget Office estimates that 24 million people will be exempt from the penalty.

This article was contributed by Amanda Garcia of GOBankingRates, a leading consumer banking and personal finance website that specializes in connecting consumers with the best interest rates nationwide.

")

{kind=link}